No economics degree required. Here is what every Berlin property owner needs to know.

Interest rates have confused and scared a lot of people over the last three years. Rates shot up, the market froze, headlines got dramatic. Now things have stabilised, and the picture is actually pretty straightforward. Let us break it down quickly.

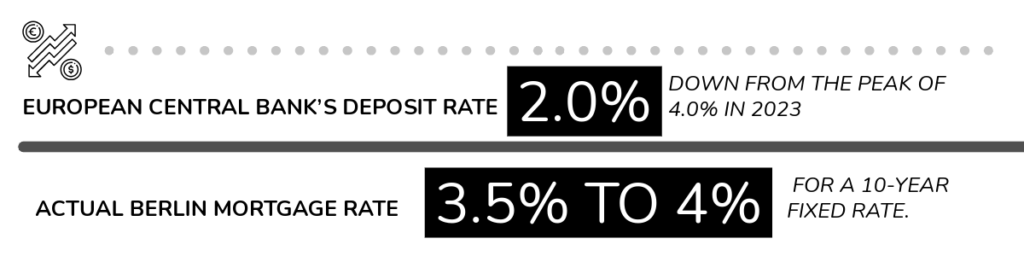

Where rates are right now

The European Central Bank’s deposit rate is currently at 2.0%, down from the peak of 4.0% in 2023 and 2024. For you as a property owner or buyer in Berlin, the number that matters most is the actual mortgage rate, which currently sits at around 3.5% to 4% for a 10-year fixed rate.

To put that in context: before 2022, mortgages were available at 1% to 1.5%. Then they jumped to 4% to 5%. Now they have come back down to a middle ground. This is not the era of free money, but it is manageable.

Is the ECB going to cut rates again?

Probably not soon, and definitely not dramatically. The ECB cut rates twice in 2025 and has since adopted a wait-and-see approach. With inflation still not fully settled at the 2% target and Germany taking on significant new debt, another big cut is not on the immediate horizon.

The most likely scenario for the rest of 2026: rates stay roughly where they are. Some experts suggest a small rate hike could even come in 2027 if inflation picks up again.

What this means if you own property

If you already have a fixed-rate mortgage, nothing changes for you until your fixation period ends. If you are coming up for refinancing in the next year or two, start planning now. The current 3.5% to 4% window may not last forever.

If you are thinking about buying, the key question is not whether rates will drop to 1% again (they will not, at least not anytime soon). The real question is whether the property you are buying makes financial sense at today’s rates. For many Berlin properties, with rents rising and vacancy near zero, the answer is still yes.

What this means if you want to sell

Higher rates reduce buyer purchasing power, which is one reason the market is more selective right now. But demand in Berlin is structural, driven by population growth and a severe housing shortage, not just by cheap credit. Well-priced properties still sell. Overpriced ones sit.

Frequently asked questions

What are mortgage rates in Germany right now in 2026?

Around 3.5% to 4% for a 10-year fixed rate mortgage. The exact rate depends on your down payment, credit profile, and lender.

Will mortgage rates go down in Germany in 2026?

A significant drop is unlikely. The ECB is in a holding pattern. Rates may edge slightly lower but a return to the ultra-low era is not expected.

Does the ECB rate affect my mortgage directly?

Not directly. German mortgage rates are more closely tied to long-term bond yields and Pfandbrief funding than to the ECB’s overnight rate. But ECB policy creates the overall environment.

The short version: rates are stable, manageable, and probably not going dramatically lower. If you have been waiting for a rate miracle before making a property decision, the data suggests that wait may not pay off.